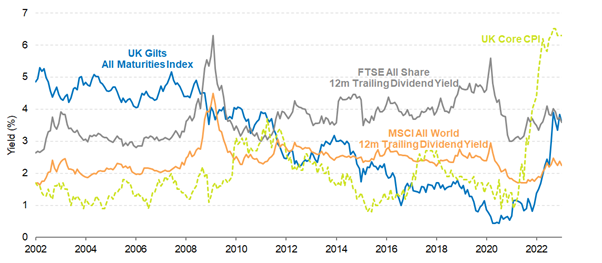

As 2023 commences in earnest, a happy by-product of last year’s volatility is the rise in bond yields. The increase in inflation across the UK, euro area, and the US, has brought bonds, including core government bonds, into play for investment strategies charged with delivering income. This has added a significant and highly useful string to our bow.

As good as economic forecasters are, they can never predict all events. In the UK for example, the rapid rotation of Prime Ministers and Chancellors in the Autumn of 2022, wasn’t in anyone’s outlook. The volatility that followed those events, especially in bond markets, was of a magnitude that sent tremors through the industry; a shake-out in LDI strategies and calls for reform to investment regulations. And of course, in the two years preceding, we had Covid and global lockdowns that until they became a reality would have been cast as the stuff of movie imaginations.

This year, well we don’t know what the universe will bring but as 2023 commences in earnest, we are well prepared. A happy by-product (and there are few) of last year’s volatility is the rise in bond yields. The increase in inflation across the UK, euro area, and the US, has brought bonds, including core government bonds, into play for investment strategies charged with delivering income. This has added a significant and highly useful string to our bow.

UK Gilts now offer a similar yield to the FTSE All Share but below core inflation. Inflation isn’t expected to stay at these levels though and the Bank of England announced earlier this month that it expects inflation to begin to fall from the middle of this year and ‘be around 4% by the end of the year and continue falling towards our 2% target after that.’

Dividends, bond yields and inflation

Past performance is not an indication of future performance

Source: Columbia Threadneedle and Bloomberg as at 25 October 2022

Our ability to hold core government bonds without sacrificing income is a welcome addition to our toolbox. With yields around 3.5 – 4%, they offer an attractive level of income alongside very useful diversification properties. We had begun to meaningfully increase our position in government bonds during the third quarter of 2022, taking advantage of the rising yields to build up duration exposures to high quality fixed income.

Policy tightening (higher interest rates and the withdrawal of quantitative easing) is feeding through into underlying economies and supply chains are realigning across the globe. This points towards disinflation and as a result, yield decreases. However, we don’t expect the decline to be rapid. Labour markets remain tight and structural themes born out of Covid, such as deglobalisation, pose upside risks to inflation.

This elevated core government bond yield environment improves not just the ability to deliver on the 4 – 4.5% yield target but also the diversification properties of our multi-asset income strategy. As assets with an increased scope to rally in a ‘classic’ risk off event as well as providing a higher level of income they provide characteristics that dramatically improve our ability to manage volatility whilst providing income as multi-asset investors.