No matter what stage of life you’re currently in, you quite possibly think that you should be saving more, wish you’d started saving sooner, and where to invest your savings to help them grow.

When considering where to invest, it can feel like you need a finance qualification to understand the options open to you, but it doesn’t have to. In this article we’ll cover some of the most common reasons for investing and how CT UK Capital and Income Investment Trust (CT UK) aims to help investors achieve these goals.

What am I saving for?

First you have to begin with the question ‘what are my future goals?’ Take the typical ‘middle-aged’ parent with teenage or older children.

You want to give them the best start in life, but it can be expensive…

If your child aspires to go to university, the costs quickly stack up, with the average university tuition fee at £9,500 per year. On top of this come living expenses, with the average accommodation costing £166 per week (1). Student loans are available, although on average parents contribute around £6,000 per year.

No sooner have young people come out of university and entered the jobs market thoughts often turn to buying a house. Over the past 25 years, the cost of housing has grown by 257% (or 92% on an inflation-adjusted basis). Rentals costs have risen too (2). For young people, paying high rent and saving for a house deposit is difficult, so the ‘Bank of Mum and Dad’ is often called upon for a gift or loan.

This level of expenditure requires long-term saving that benefits from growth, to maximise the potential long-term investment increase, whilst also providing an income to help cover some of the expenditure if required.

Where can you find that coupling? Well CT UK Capital and Income Investment trust aims to grow your investment whilst paying a dividend 4 times a year*, which can be realized to pay for tuition fees for example or reinvested for to boost the long-term growth of your investment.

CT UK has a strong record of growing investments and not only paying a dividend but one that has increased annually for over 50 years, as highlighted by the awarding of the AIC Dividend hero status by the Association of Investment Companies (link), although there is not a guarantee that the dividend will continue to increase.

The growth CT UK has delivered outweighs both a savings account and a passive investment which follows the FTSE All-Share Index. For example, £1,000 invested when CT UK launched in 1992 would have yielded £2,501 in gross income, assuming dividends had not been reinvested. This compares to just £1,112 paid out on the FTSE All-Share Index based on the annual dividend yield (source: Refinitiv Eikon), and £1,185 earned from a Savings Account paying the Bank of England base rate over the same period (source: Bank Rate history and data | Bank of England Database)**.

But it’s not all about the children

Retiring with the lifestyle we desire is often a key saving motivator for all of us.

How will you cover that once in a lifetime cruise, golf trips, and general rise in the cost of living? What is more, by virtue of our life expectancy increasing, the cost of retirement increases.

So, whilst your pension is the traditional way of supporting your retirement, to help meet your needs, supplementary investing and income has never been more important.

What are the considerations for an investment focusing on retirement? Well, there is no topic more pertinent than volatility, and retirement investing ought to be able to grow over the long term and weather multiple storms.

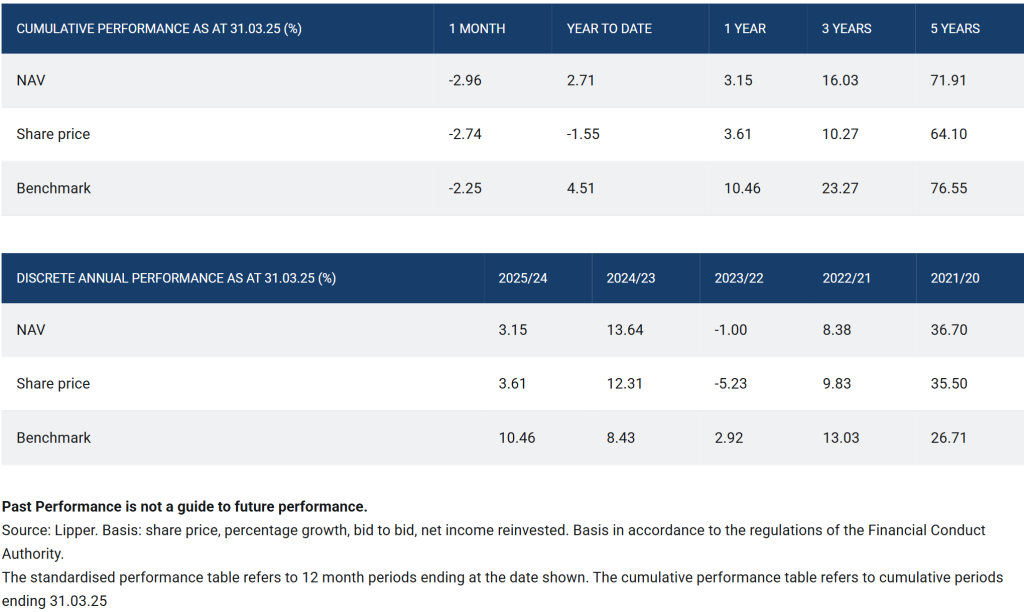

Looking at an Investment Trust’s strategy for example, you want to see a focus on long term. CT UK concentrates on carefully identifying companies that are growing and profitable today and have the strong, sustainable foundations to be able to continue that profitable growth into the future. Since its inception, CT UK’s long-term performance has been ahead of industry benchmarks (eg FTSE All Share) for capital growth. Notably, this period of time included some rather large storms: the 2000 Dot-com bubble, the 2008 financial crisis, and more recently Covid-19.

How does CT UK Capital and Income Investment Trust achieve

its success?

CT UK Capital and Income Investment trust has been searching out the very best of the UK’s large and medium sized businesses since 1992 to give its shareholders access to a range of quality UK stocks in one place. It carefully identifies companies that are growing and profitable today and have the sustainable foundations that have the potential to continue that profitable growth into the future.

The trust chooses to invest in companies that it strongly believes in. Most of them generate much of their revenues outside the UK, which means shareholders benefit from international growth and greater geographic exposure. Through the careful selection of UK companies and diversified portfolio construction, the trust has been able to increase its dividend every year since its launch, through the market’s ups and downs.

Why consider UK equities?

The UK equity market is particularly interesting at the moment as it is seen as being undervalued, and thus potentially offering great opportunity.

There are several reasons for this perceived undervaluation. In the last few years, the UK equity market has experienced a period of volatility, initially seeing a downturn due to Brexit uncertainty and the pandemic, and then facing the headwind of surging inflation, bringing about strongly rising interest rates and bond yields. This has meant that valuations for many companies and the market as a whole are at low levels compared to their own historic ranges and compared to international peers. The economy is now on a more stable footing with real wage growth, inflation stabilising

and interest rates gradually reducing.

Finally

One-third of adults wish they’d started saving sooner (3), so take the chance to get focused on your savings plans. As they like to say, the best time to start investing was yesterday, but the next best time is today.

(3) https://www.independent.co.uk/money/children-isa-people-scotland-northern-ireland-b2432996.html

Investment risks

*There is no guarantee that dividends will continue to increase.

**Past performance is not an indicator of future returns

The value of your investments and any income from them can go down as well as up and you may not get back the original amount invested.

Gearing is used for investment purposes to obtain, increase or reduce exposure to an asset, index or investment. The use of gearing can enhance returns to investors in a rising market, but if the market falls the losses may be greater.

Issued by Columbia Threadneedle Management Limited and approved for distribution 06/03/2025.